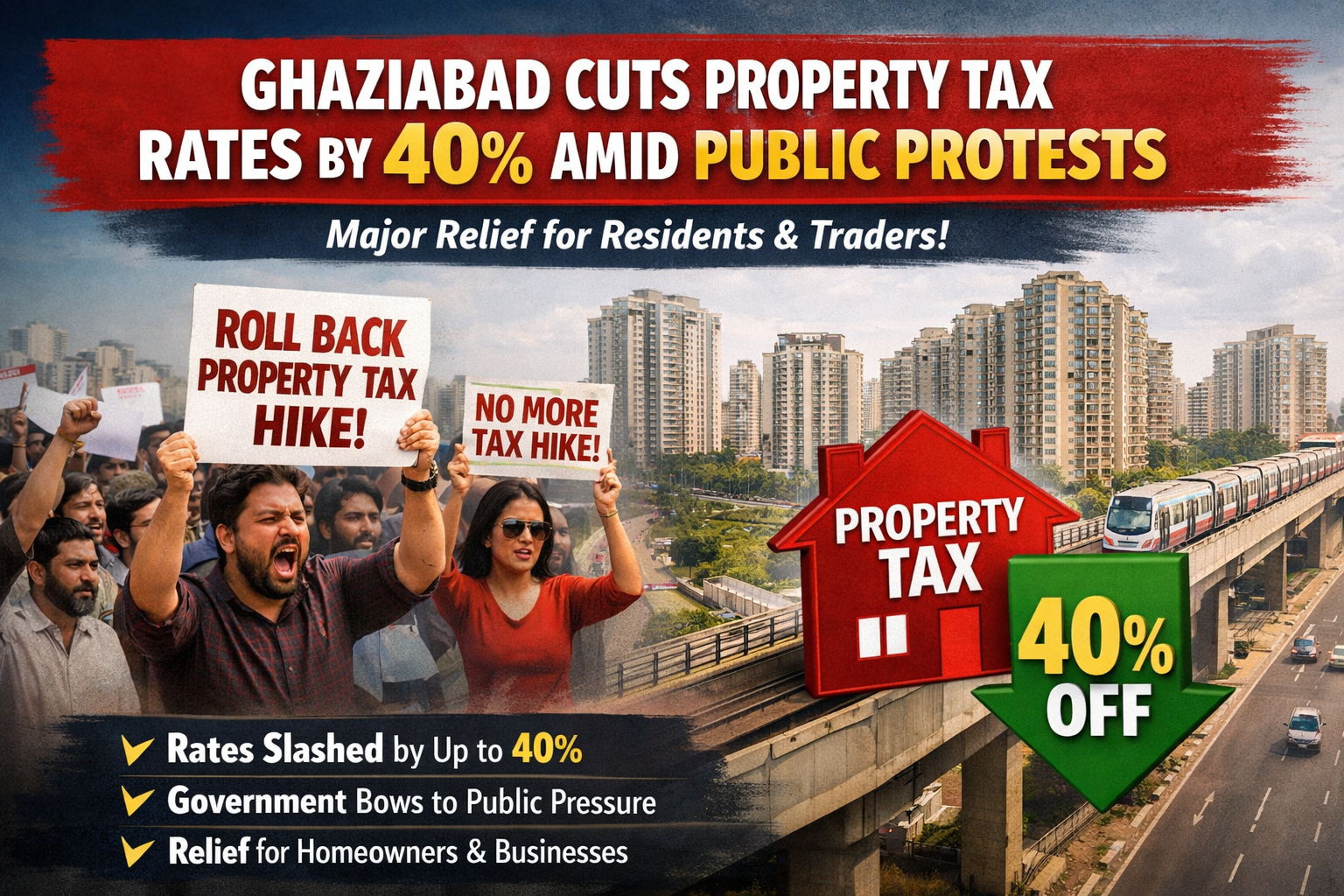

India Housing Sales Fall Below 100,000 Units.

Housing sales across India’s top nine cities fell below the 100,000-unit mark after 18 quarters in January–March 2026.

Housing sales across India’s top nine cities fell below the 100,000-unit mark after 18 quarters in January–March 2026, with sales at 98,761 units. Sales declined 13 percent year-on-year and six percent quarter-on-quarter, while new housing launches dropped 19 percent annually and eight percent sequentially.

India’s residential real estate market has entered a phase of visible moderation, as housing sales across the country’s top nine cities slipped below the 100,000-unit mark for the first time in 18 quarters during the January–March 2026 period. The total number of units sold stood at 98,761, reflecting a 13 per cent decline on a year-on-year basis and a 6 per cent drop compared to the previous quarter. This shift signals a pause in the strong post-pandemic momentum that had defined the housing sector over the past few years, indicating a transition rather than a complete slowdown.

The dip in sales has not occurred in isolation but is closely linked to a significant contraction in new housing supply. During the same quarter, new project launches fell to 92,411 units, marking a sharp decline of 19 per cent year-on-year and 8 per cent quarter-on-quarter. This reduction in fresh inventory has played a critical role in limiting buyer choices and, consequently, transaction volumes across major urban markets. The data suggests that the current slowdown is largely supply-driven rather than a result of weakening demand fundamentals.

A closer look at city-level performance reveals a mixed landscape. Delhi-NCR emerged as a notable outlier on the supply side, recording 17,227 units launched during the quarter. This represented an 89 per cent increase compared to the same period last year and an 8 per cent rise sequentially, making it the only major market to witness a significant growth in new launches. Despite this surge in supply, absorption levels in the region remained relatively subdued, largely due to the dominance of high-ticket housing projects that impacted affordability for a broader segment of buyers.

Bengaluru, on the other hand, continued to demonstrate resilience and emerged as one of the strongest-performing markets. The city recorded robust housing activity with both sales and launches maintaining relative stability. While new launches stood at 17,782 units, reflecting a 10 per cent quarter-on-quarter increase, they were still lower by 24 per cent compared to the previous year. In terms of sales, Bengaluru led among the top cities, indicating that demand remained intact where supply was aligned with buyer preferences across price segments.

Chennai presented another contrasting trend. The city witnessed a sequential rise in launches by 12 per cent, reaching 2,909 units during the quarter. However, on a year-on-year basis, supply fell sharply by 62 per cent, highlighting the broader issue of constrained development activity. Similar patterns were observed across several other metropolitan markets, where both sales and supply experienced declines, reinforcing the notion of a widespread inventory crunch affecting the overall market performance.

Quick Enquiry

Related News & Updates